Strategy Execution Template - Master PatternThis script is a template to execute your strategy with Stop Loss and Take Profit and showing Trades.

Then, you can write your strategy without taking care of Stop Loss and Take Profit method.

3x Fixed Percent Stop Loss, Trailing Percent Stop Loss, Trailing ATR Stop Loss, Tailing HHLL Stop Loss

3x Fixed Percent, Take Profit

"stop loss" için komut dosyalarını ara

Compound strategyIn this strategy, I looked at how to manage the crypto I bought. Once we have a little understanding of how cryptocurrency is valued, we can manage the coins we have. For example, the most valuable coin in a coin is to sell when it is overvalued and re-buy when it is undervalued. Furthermore, I realised that buying from the right place and selling at the right time is very important to make a good profit. When it says sell, it's divided into several parts.

1. When the major uptrend is over and we are able to make the desired profit, we will sell our holdings outright.

2. Selling in the middle of a down trend and buying less than that amount again

3. When a small uptrend is over, sell the ones you bought at a lower price and make a small profit.

The other important thing is that the average cost is gradually reduced. Also, those who sell at a loss will reduce their profit (winning rate), so knowing that we will have a chance to calculate our loss and recover it. I used this to write a strategy in Trading View. I have put the link below it. From that we can see how this idea works. What I did was I made the signal by taking some technical indicators as I did in the previous one (all the indicators I got in this case were directional indicators, then I was able to get a good correlation and a standard deviation. I multiplied the correlation and the standard deviation by both and I took the signal as the time when the graph went through zero, and I connected it to the volume so that I could see some of the volume supported by it.)

Now let me tell you a little bit about what I see in this strategy. In this I used the compound effect. That is, the strategy, the profit he takes to reinvest. On the other hand, the strategy itself can put a separate stop loss value on each trade and avoid any major loss from that trade. I also added to this strategy the ability to do swing trading. That means we can take the small profits that come with going on a big up trend or a big down trend. Combined with Compound Effect, Stop Loss and Swing Trading, I was able to make a profit of 894% per annum (1,117.62% for 15 months) with a winning rate of 80%. Winning rate dropped to 80% because I added stop loss and swing trading. The other thing is that I applied DCA to this in both the up trend and the down trend (both). That was another reason for me to make a good profit. The orange line shows how to reduction of costly trade. The yellow line shows the profit and you can see that the profit line does not go down during the loss trades. That's because I want to absorb the loss from that trade.

Unicorn Quant Strategy [Astride Unicorn]Deeply customizable trading algorithm with instant back-testing. Its position management and trading signals engines emulate every step of the trading process and display all the actions on the chart. For example, the algorithm shows when to enter or partially close a position, move stop-loss to breakeven, etc. The trader can use these signals in their decision-making and replicate these actions in their trading terminal. The script can also send real-time alerts to the user’s Email.

The trading signals feature calculates entry signals for momentum and trend trading. The calculation is based on trend filtering using our custom filter based on rolling historical volatility. The historical volatility is used to distinguish the market regime and determine the current trend direction. In its calculations, the algorithm uses linear regressions instead of averaging. As our practice shows, it helps to reduce signal lag while keeping the number of false signals low.

HOW TO USE

Set stop-loss and up to three take-profit levels, choose rules for moving the stop-loss level, adjust sensitivity of the entry signals and see the back-test result immediately. If the performance of the strategy satisfies you, proceed with the forward-testing or live-trading.

When using this script, please, keep in mind that past results do not necessarily reflect future results and that many factors influence trading results.

SETTINGS

Use Starting Date - when the flag is turned off, the algorithm uses all available pricing data to calculate back-tests; when turned on, back-tests start from a starting date the user can select in the setting below.

Starting Date - sets a starting date for back-testing.

Trading Signals

Trade Length - defines the length of the trades the algorithm tries to calculate entry signals for. Recommended values are from 1.0 to 6.0.

Sensitivity - controls the sensitivity of the trading signals algorithm. The sensitivity determines the density of trading signals and how close the trailing-stop levels follow the price. The higher the value of this parameter is, the less sensitive the algorithm is. High values of the Sensitivity parameters (100-500) can help to withstand large price swings to stay in longer price moves. Lower values (10-100) work well for short- and medium-term trades.

Signals Type - In the Signals Type dropdown list, there are two options: Market Timing and Market Bias. Market timing is a type of trading signaling when the algorithm tries to find a perfect moment to enter and exit a trade. Market Bias is the type of trading signaling when the algorithm tries to be in a position all the time. When a trade is closed, the algorithm determines a direction to which the market is currently “biased” and immediately opens a trade in this direction.

Position Management

SL - sets stop-loss level measured as a percentage of the trade entry price

TP1, TP2, TP3 - sets take-profit levels measured as a percentage of the trade entry price

Close % at TP1, Close % at TP2, Close % at TP3 - Sets portions of the open position(as a percentage of the initial order size) to close at each of the TP levels

At TP1 move SL to, At TP2 move SL to - Sets the rules for moving stop-loss level in an open trade to protect the floating profit

Dashboards

Active Position Information - turns on/off a dashboard that shows the current SL and TP levels for the active position.

Recommended SL,TP Settings - turns on/off a dashboard that shows recommended settings for the SL and TP levels.

SuperTrend Multiple Risk Management SystemThis is an improved SuperTrend strategy that makes use of multiple types of risk management options.

We have for example :

1. Take profit and stop loss levels based on support and resistence created with RSI and Pivot Lines(dynamic)

For example, if we have an oversold level and a pivot low , we can take that low point for support.(or resistence for short)

If instead we have an overbought level and a pivot high, we can take that high point for resistence.(orsupport for short)

2. Take profit and stop loss levels based on swing low and swing high points calculated with highest high and lowest low function(dynamic)

For example we take the lowest point in the last 100 candles. We calculate the distance from the current point to that one, and we apply this value as a take profit point. Same for stop loss

3. Take profit and stop loss levels based on % movements(fixed)

For example we have a tp or sl of 10%. If either of them make a movement of 10% from the entry point, they will get triggered.

4. Break even stop loss once the asset moves certain % in our direction.

For example we have a long breakeven of 5%. If the asset moves 5% in our direction, we move the stop loss on the entry point so if the trade pullback and crosses with this point it will exit from the trade.

Notes:

All the exits from the strategy are happening at the end of the candle close, since we are checking if inside the current candle we cross with either high or low of the candles parts the set prices from any of the above options.

At the same time we can combine multiple of them into one, and we can either exit based on which one was hit first, or use a quantity reduction of the trade and exit multiple times when we hit any of the levels.

This tool is for educational purpose only.

Its main purpose is to show the difference between having a risk management or without.

For example on this scenario of BTC USD 4h, I found out that the drawdawn was reduced by more than half when using different type of risk management, compared to not use one at all, while at the same time increasing the profits by a huge margin.

[Herif's] Harmonic Patterns ProjectionBullish and bearish 5-point patterns are based on various Fibonacci retracement levels and signify potential reversal zones (PRZ).

As they become 0%-80% complete, the dashed-line pattern will appear, displaying the PRZ and giving you time to prepare for a reversal.

Different combinations of specific fib retracements and extensions result in different patterns, and each is named for identification.

Bullish patterns signify a potential turn to the upside are colored green.

Bearish patterns signify a potential turn to the downside are colored red.

1- Live harmonic patterns which are still in trade with XABCD and ratio with labels.

2- Entry, Stop and Target levels on chart for all patterns.

in Settings:

Error Percent - This is error tollerance for matching pattern ratios. Cannot expect price ratios to be exactly as per books. Hence, adding few error tolerance will help identify patterns better. In this indicator defatult 1%

When there are multiple patterns on chart, Entry, Stop, and Target labels and lines are created with specific distance from each other to provide clarity to the users.

Trailing and Targets

1-Trailing Start Stage - Defines when to start trailing stop-loss. It is recommended to set this value to either Target 1 or Target 2. Disabling the trailing or setting too far away may lead to being in trade on ranging market for too long. This may also result in drawing errors related to distance from current bar.

2- Custom Target Levels - Target and stop levels are set to optimal values based on individual patterns. If you want to override these levels, use the available input option to override targets and chose your custom Target1, Target2, Target3 and Target4

All Pending Patterns you can enable or disable

Classic Patterns : Gartley , Bat, Butterfly , Crab , Deep Crab , Cypher , Shark , Nenstar

Anti Patterns: Anti Nenstar, Anti Shark , Anti Cypher , Anti Crab , Anti Butterfly , Anti Bat, Anti Gartley , Navarro 200

This is a Strategy version of indicator below

[Herif's] Harmonic PatternsFollowing things are displayed by default on the chart with harmonic patterns strategy. It can be use with automate trading platforms 3commas, zignally, frostybot, alertatron, wunderbit etc...

Bullish and bearish 5-point patterns are based on various Fibonacci retracement levels and signify potential reversal zones (PRZ).

As they become 80% complete, the dashed-line pattern will appear, displaying the PRZ and giving you time to prepare for a reversal.

Different combinations of specific fib retracements and extensions result in different patterns, and each is named for identification.

Bullish patterns signify a potential turn to the upside are colored green.

Bearish patterns signify a potential turn to the downside are colored red.

1- Live harmonic patterns which are still in trade with XABCD and ratio with labels.

2- Position Entry, Stop and Target levels on chart for all patterns.

3- Trades Stat table - Waves stat tables

in Settings:

Error Percent - This is error tollerance for matching pattern ratios. Cannot expect price ratios to be exactly as per books. Hence, adding few error tolerance will help identify patterns better.

When there are multiple patterns on chart, Entry, Stop, and Target labels and lines are created with specific distance from each other to provide clarity to the users.

Trailing and Targets

1-Trailing Start Stage - Defines when to start trailing stop-loss. It is recommended to set this value to either Target 1 or Target 2. Disabling the trailing or setting too far away may lead to being in trade on ranging market for too long. This may also result in drawing errors related to distance from current bar.

2- Custom Target Levels - Target and stop levels are set to optimal values based on individual patterns. If you want to override these levels, use the available input option to override targets and chose your custom Target1, Target2, Target3 and Target4

All Patterns you can enable or disable

Classic Patterns : Gartley, Bat, Butterfly, Crab, Deep Crab, Cypher, Shark, Nenstar

Anti Patterns: Anti Nenstar, Anti Shark, Anti Cypher, Anti Crab, Anti Butterfly, Anti Bat, Anti Gartley, Navarro 200

I will plan some updates and i will post some screen shots for settings as soon as possible.

Bot go_up DD_long/shortHello!

This strategy is based on the double bottom pattern - for entering a long position / double top-short

A double bottom pattern is formed when two price bottoms are relatively at the same level and the top acts as resistance. This pattern appears at the end of a downtrend and signals a reversal.

A double top is a bearish reversal pattern that signals the end of an uptrend. It is formed by two price highs forming at the same level and a notch line that acts as local support.

As history and practice show, the double bottom pattern works better. Moreover, in a bull market.

You can include only long or only short. BUT while there is a long, a short position will not be opened, in fact, with a long as well.

You can use reverse trade, one coin at a time.

DESCRIPTION:

// LOGIC ENTRY:

Period for short and long positions-to search for double bottom as well as double top. the more, the less false.

Change liong and short-channel width for pattern search separately for long and short.

General shift-the overall width of the channel, which changes equally at once for long and short

By default, quiet settings for tf 5 minutes are applied!

You can choose the settings you like.

// AMOUNT(USDT) FIRST ORDER AND > % NEXT

In the first column, indicate the amount, in the second, how many percent the next order will be more than the previous one.

// EXIT SETTINGS

Closing a trade by RSI when it reaches the level specified in the settings (but in the negative, the trade will never be closed, even if the condition is triggered)

Using a percentage to exit a trade + stop loss. (Put a stop order 1000+ on the market can be anything, especially if you use spot trading)

PS: in order to use the RSI output at a certain level, put a checkmark on the desired one, and also check the percentage box and indicate a take on the percentage 10-20 +)

// MARTINGALE GRID

If there is a check mark, then the grid is used.

Use all signals?

If yes, then there will be no limit on inputs from logic

If the checkbox is not checked, then you can limit the entries from the strategy logic by the specified percentage.

Grid, the next order, when decreasing by a certain percentage, an order when decreasing by the percentage that will be specified (after entering from the logic, when the next signal appears, the grid will be counted from the beginning)

PS: orders are not automatically placed, if the conditions are triggered, then the entry is only at the next bar (within the TV, it is not possible to add orders immediately, but most often, in case of straits, for the better)

// FILTER SETTINGS

The filter consists of a series of popular, averaged oscillators

//DATA RANGE

You can see the results for the selected period

//

CALCULATION OF ORDERS AND MARGIN (FOR INFO ONLY)

The number of orders is the number of entries (you must always have the same number of orders in the arguments and in the properties !!)

- in the aruments for understanding, in the properties - it does not matter how much it will cost there, so many inputs will be!)

-leverage is created to calculate the margin

When you change these parameters, you will understand how much money is required in general and what maximum drawdown can be allowed

Green line-take, lower-stop-order.

To use algo trading, in fact, you need to use a script, in the service through which you will transmit a signal through webhooks, you need to select the amount.

{{strategy.order.contracts}}

ОПИСАНИЕ НА РУССКОМ

//ЛОГИКА ВХОДА:

Период для шорт и лонг позиций, сдвиг для шорта лонга, также общий

По умолчанию применены спокойные настройки для тф. 5 минут.

Вы можете самостоятельно подбирать настройки, основываясь на прошлые результаты

//СУММА ВХОДА В ЮЗДТ +МАРТИНГЕЙЛ:

В первой графе указываете сумму , во второй -на сколько процентов следующий ордер будет больше предыдущего.

//НАСТРОЙКИ ВЫХОДА ИЗ СДЕЛКИ

Закрытие сделки по RSI, когда достигнет уровня, указанного в настройках ( но в минус сделка не будет закрыта никогда, даже если условие сработало)

Использование процента для выхода из сделки+ стоп приказ.( Ставьте стоп-приказ 1000+ на рынке может быть всякое, тем более, если используете спотовую торговлю)

ПС: для того, чтобы использовать выход по RSI по определенному уровню, поставьте галочку на нужный , а также поставьте галочку по проценту и укажите тейк по проценту 10-20+)

//НАСТРОЙКИ СЕТКИ

Если стоит галочка-то сетка используется.

Использовать все сигналы?

Если да, то лимита по входам от логики не будет

Если не стоит галочка, то можно ограничить входы от логики стратегии, на указанный процент.

Сетка, следующий ордер, при снижении на определенный процент-след ордер при снижении на тот процент, который будет указан ( после входа от логики , при появлении следующего сигнала сетка будет считаться с начала)

ПС: ордера автоматически не ставятся, если сработали условия, то вход, только на следующем баре ( в рамках ТВ, нет возможности добавить сразу ордера, но чаще всего, при проливах-к лучшему)

//НАСТРОЙКИ ФИЛЬТРА

Фильтр состоит из серии популярных, усредненных осцилляторов.

//

БЭКТЕСТИНГ

Можете посмотреть результаты за выбранный промежуток

//

ПИРАМИДИНГ (исключительно для расчета)

Количество ордеров-это количество входов ( у вас всегда должно быть одинаковое количество ордеров в агрументах и в свойствах!!)

-в аргументах для понимания, в свойствах -важно, сколько там будет стоить-столько входов и будет!)

-плечо создано для расчета маржи

При изменение данных параметров Вы будете понимать сколько потребуется средств в общем и какую максимальную просадку можно допустить

Зеленая линия-тейк, нижняя-стоп-приказ.

Для использования алго-трейдинга, собственно так и нужно использовать скрипт, в сервисе, через который Вы будете передавать сигнал через веб-хуки , Вам нужно выбрать количество.

{{strategy.order.contracts}}

Удачных трейдов, друзья!

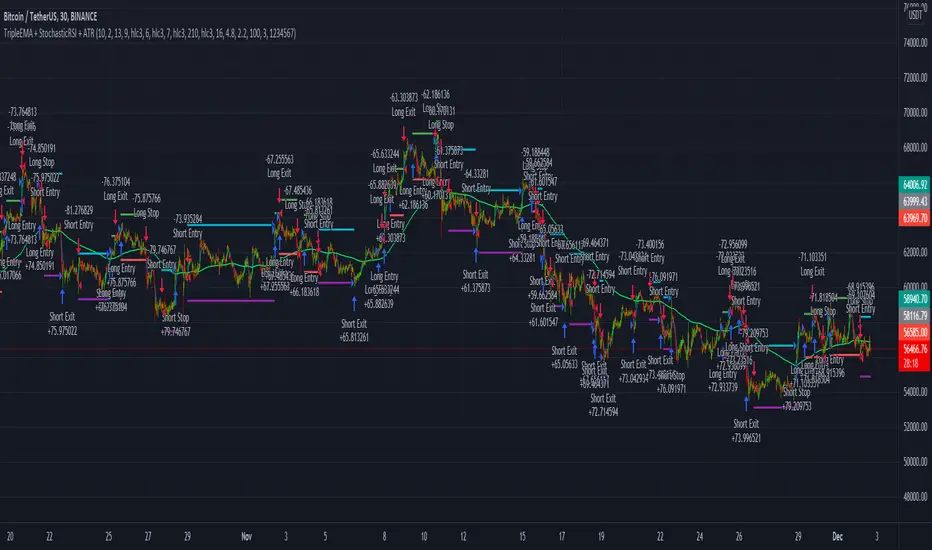

TripleEMA + StochasticRSI + ATR Scalping Strategy by TradeSmartCOINBASE:BTCUSD Hello everyone and welcome to our second script release!

This script is one of many upcoming scripts. This one is a test for us, how it works, how you guys like this kind of stuff, and for feedback what we should change/improve at.

So feel free to comment any suggestions you have.

SCRIPT IS OPTIMIZED FOR:

BTC/USD (Coinbase) 15 minute timeframe

(Keep in mind default settings does not include trading fees, you can set it at the properties)

I recommend using this script on a trading exchange where the fees are extremely low or on an exchange where you get paid to place limit orders.

(I am not a financial avdvisor and none of this is financial advice.)

Now you can modify the following:

Stochastic RSI

3 different EMA

Length of ATR (for stop loss and take profit)

Stop Loss and Take Profit Risk to Reward ratio

Choice between Capital Risk on each trade or Risk of % of Capital

Allowing Short/Long entries only

Limit between dates

Trading days 1-7

We will update the script with more and more features taking in consideration your requests.

Hope you like it! Don't forget to let us know what we should change or improve. Thanks, and have a great day!

STRATEGY ENTRY RULES

LONG

When EMAs are lining up (meaning for ex. 400 < 13 < 7), and the Stochastic RSI crosses upwards (meaning blue line crosses orange upwards), then go long.

SHORT

When EMAs are lining down (meaning for ex. 7 < 13 < 400), and the Stochastic RSI crosses downwards (meaning blue line crosses orange downwards), then go short.

TAKE PROFIT

When price hits the exit price (calculated from stop loss with the risk ratio)

STOP LOSS

When price hits stop loss then exit the position.

QUANTITY TO BUY (Risk per Trade % or Capital %)

Risk Per Trade % attribute: we can set how much money we want to risk on one trade. Meaning that if we lose that particular position, then a Risk Per Trade % value of our equity will be lost.

Example: if you set the Risk Per Trade % to 1 % and you have a 100$ account balance, then if you loose the trade you will loose 1$ max.

Capital % we can set with how big % of our capital we want to enter into a position. Meaning that we enter with a set % of our capital.

Example: if you set the Capital % to 1 % and you have a 100$ account balance, then you will enter the position with 1$.

First Release Settings: (2021-10-25) for BTC/USD (Coinbase) 15 minute timeframe

Stochastic RSI settings: (Not displayed in the script. If you want to see it you have to add it separately.)

K: 3

D: 2

RSI Length: 6

Stochastic Length: 16

RSI Source: hlc3

EMA 1: 5

Source One: Close

EMA 2: 12

Source Two: Close

EMA 3: 215

Source Three: Close

Length of ATR: 16

Stop Loss Multiplier (risk): 3.6

Exit Price Multiplier (reward): 1

Risk Percentage: 3

Allow Long Entries: yes

Allow Short Entries: yes

Valid Trading Days: 1234567

The valid trading days of the Limit Trading Time feature. Numbers represent the days: Sunday (1), Monday (2), Tuesday (3), …, Saturday (7)

If you like this one, follow for more scripts! Thank you for your support!

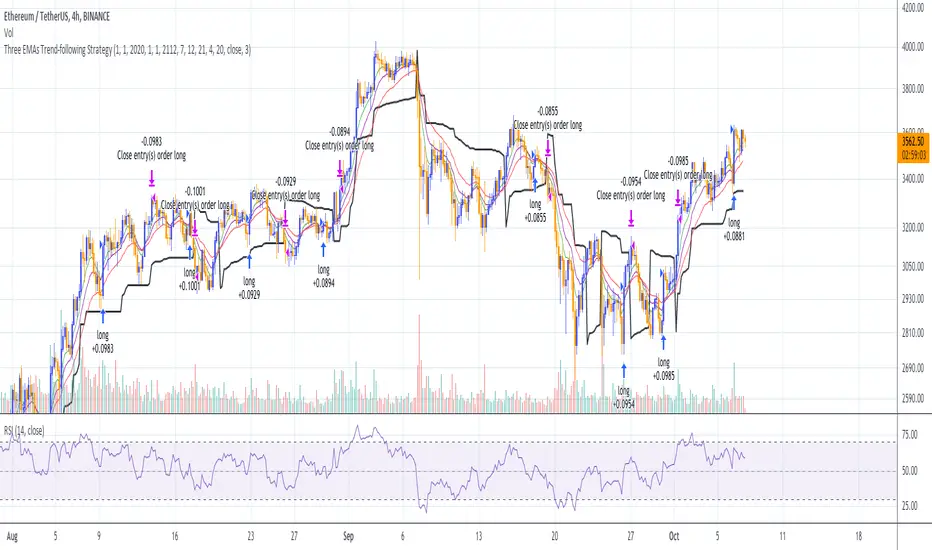

Three EMAs Trend-following Strategy (by Coinrule)Trend-following strategies are great because they give you the peace of mind that you're trading in line with the market.

However, by definition, you're always following . That means you're always a bit later than your want to be. The main challenges such strategies face are:

Confirming that there is a trend

Following the trend, hopefully, early enough to catch the majority of the move

Hopping off the trade when it seems to have run its course

This EMA Trend-following strategy attempts to address such challenges while allowing for a dynamic stop loss.

ENTRY

The trading system requires three crossovers on the same candle to confirm that a new trend is beginning:

Price crossing over EMA 7

Price crossing over EMA 14

Price crossing over EMA 21

The first benefit of using all three crossovers is to reduce false signals. The second benefit is that you know that a strong trend is likely to develop relatively soon, with the help of the fast setup of the three EMAs.

EXIT

The strategy comes with a fixed take profit and a volatility stop, which acts as a trailing stop to adapt to the trend's strength. That helps you get out of the way as soon as market conditions change. Depending on your long term confidence in the asset, you can edit the fixed take profit to be more conservative or aggressive.

The position is closed when:

The price increases by 4%

The price crosses below the volatility stop.

The best time frame for this strategy based on our backtest is the 4-hr. Shorter timeframes can also work well, although they exhibit larger volatility in their returns. In general, this approach suits medium timeframes. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

You can execute this strategy on your favourite exchange at coinrule.com

3Commas DCA Bot Strategy v1.0Introduction

The strategy attempts to implement a majority all of the settings found on the 3Commas DCA Bot setting page that can be implemented within a TradingView indicator. Specifically, it will implement the "Open new trade ASAP" and "Trading View Custom Signal" deal start conditions. In this way, you can leverage the power of TradingView's backtester to model your settings and analysis past performance as well as leverage TradingView's alert notification subsystem to send Deal Start and Close signals to 3Commas using almost any of the thousands of scripts found in the Public Library (see "What does it do and how does it do it?" section below for more information on how to do this using the RSI indicator as an example).

How is it original and useful?

This strategy is unique in that it's the only one (as of the initial publications) that can handle 28 out of 32 bot settings (88% coverage) that are found on the 3Commas bot settings page. In addition, because it is a TradingView script, you will benefit from the following:

Model your bot's configuration using the backtester on any timeframe and evaluate its performance using the chart's history.

View a table of detailed statistics pertaining to deals started and completed, win/loss rates, daily P&L, true max drawdown, and detailed statistics on bars in deal along with safety orders filled.

View a table of "Used amount for each step" as presented in 3Commas as well.

Ability to link to almost any TradingView chart indicator that provides a single data point for buy/sell signals.

Make use of the 3Commas TA Start Conditions indicator to emulate the 3Commas built-in indicators for further performance evaluation with the backtester.

How does it compare to other scripts in the Public Library?

This strategy offers a very detailed, comprehensive settings and maybe the only one (as of the initial publication) that can handle 28 out of the 32 bot settings that are found on the 3Commas bot settings page (that can be handled within TradingView, because some cannot be modeled due to chart and language constraints). Specifically, the following 3Commas bot settings and inputs are addressed with asterisks denoting specific limitation due to TradingView's platform architecture and/or constraints:

Main settings

✅ Name

❌ Exchange* (Not handled since it is inherited from chart)

⚠ Bot type* (Only Single-pair because you simply apply the indicator to as many pairs you desire in separate charts to simulate a Multi-pair setting)

Pairs

❌ Pairs* (Not handled since it is inheriting the symbol from the chart)

Strategy

✅ Strategy

❌ Profit currency* (Not handled since there is no equivalence in TradingView)

✅ Base order size / unit

✅ Safety order size / unit

✅ Start order type

Deal start condition

⚠ TradingView* (You can modify the "Technical Rating" indicator by TradingView to output a signal yourself like @TheTradingParrot has done in the TV signal for DCA backtest script)

⚠ QFL* (See Quickfingers Luc's Base Breaking Strategy v2.5 - 3Commas Edition for an alternative)

❌ Manually/API* (Not handled since there is no equivalence in TradingView)

✅ Trading View custom signal

✅ Open new trade asap

Take profit

✅ Take profit (%)

✅ Take profit type

✅ Trailing

⚠ Trailing deviation* (modified to handle TradingView's broker emulator properly)

Stop loss

✅ Stop Loss (%)

✅ Stop Loss action

⚠ Stop Loss timeout* (modified to use "bars" as the unit of measure)

Safety orders

✅ Max safety trades count (a total of 100 safety orders are supported!)

⚠ Max active safety trades count* (Not handled since there is no equivalence in TradingView)

✅ Price deviation to open safety orders (% from initial order)

✅ Safety order volume scale

✅ Safety order step scale

Advanced settings

✅ Don't start deal(s) if the daily volume is less than

✅ Minimum price to open deal

✅ Maximum price to open deal

⚠ Deal start delay (QFL and standard TV signals only)* (modified to use "bars" as the unit of measure)

✅ Cooldown between deals

✅ Open deals & stop

Close deal after timeout

⚠ The time after which, deal will be closed automatically* (modified to use "bars" as the unit of measure)

In addition to the above inputs, the script will also support the same output data points that are found on the bot settings page, which are:

Assistant

✅ Balance

✅ Max amount for bot usage (Based on current rate)

✅ Max safety order price deviation

✅ % of available balance to be used by the bot

Table (Used amount for each step)

✅ Order No.

✅ Deviation %

✅ Order Size (Base currency)

✅ Order Volume (Quote currency)

✅ Price

✅ Average price

✅ Required price

✅ Required change

✅ Total Size (Base currency)

✅ Total Volume (Quote currency)

What does it do and how does it do it?

When applied to the chart for the first time, the default settings will work to execute the "Open new trade asap" deal start condition using a take profit of 4%, a base order size of 1.335% of equity (initial capital + net profit), a safety order size of 2.003% of equity (initial capital + net profit), a safety order volume scale of 1.5, a safety order step scale of 1.21, and a max safety trades count of 8. With these settings, as you scroll through the chart's history you should see price action crossing the DCA layers (denoted with blue triangles), and a green take-profit price line will render (with green triangle denoting the crossings). Lastly, in the upper-right corner of the chart the table of DCA statistics will render showing you all the gathered data that took place since the chart's starting history until the current time.

Using the "TV Custom Signal" section will allow you to "link" other chart indicators to supply "Start" and "Close" signals for the script. For example, here's how you can use the standard RSI indicator to generate an entry signal:

1) Add the stock RSI indicator and configure it to your desire.

2) Select the "RSI" indicator in the "Chart/Indicator Data Point" input.

3) Select "Chart/Indicator Data Point" in the "Start Deal When" input.

4) Select "Less Than" in the "Is" input.

5) Select "Custom Value(s)" in the "The Value Of" input.

6) Enter "25" in the "Custom Value 1 (Single or Lower Bound)" input.

7) Select "Trading View Custom Signal" in the "Open new trade" input (in the DEAL START CONDITION section).

8) Lastly, check the checkbox with a horizontal straight line above the "Start Deal When" input.

This means that the indicator will start a deal when the "RSI indicator" is "Less Than" the value of "25".

Strategy Results

The default settings are designed to ensure that the indicator will render chart elements when first loaded as well as to allow the backtester to gather order executions and display performance summary. The chart above is is using $10,000 initial capital, a commission rate of 0.1% for both entries and exits, and a 1 tick slippage setting. It is also using 3.22581% of the equity for the Base Order Size, 6.45161% of equity for the first Safety Order Size. The Maximum Safety Trade Count is 4 with a Safety Order Volume Scale of 2, a Safety Order Step Scale of 1.53, Price Deviation To Option Safety Orders at 5.3, and a take profit of 4.5% with Trailing turned on at a deviation of 1.5%. All other settings are defaults.

It is recommended that the indicator be "tuned" for your specific market in order to best implement the strategy and obtain better desirable results. You do so by using the backtester and statistics table and observe the output values and learn how the indicator is performing in the chart history. Using this information, you can adjust the settings accordingly until you find the settings acceptable to your trading goals and risk tolerance.

Always keep in mind that past performance may not be indicative of future results. Settings that seem favorable for one market may be found to be disastrous in another. Therefore, do take the time needed to understand how the settings will behave with the given chart symbol.

Enjoy! 😊👍

How to obtain access to the script?

You have two choices:

Use the "Website" link below to obtain access to this indicator, or

Send us a private message (PM) in TradingView itself.

Optimized Keltner Channels SL/TP Strategy for BTCThis strategy is optimized for Bitcoin with the Keltner Channel Strategy, which is TradingView's built-in strategy. In the original Keltner Channel Strategy, it was difficult to predict the timing of entry because the Buy and Sell signals floated in the middle of the candle in real time. This strategy is convenient because if the bitcoin price hits the top or bottom of the Keltner Channel and closes the closing price, you can enter Buy or Sell at the next candle start price. In addition, this strategy provides Stop Loss and Take Profit functions to maximize profit.

_________________________________

Recommended settings are below.

- length: 9

- multiplier: 1

- source: close

- (v) Use EMA

- Bands Style: Average True Range

- ATR Length: 19

- Stop Loss (%): 20

- Take Profit (%) : 20

_________________________________

- length: 9

- multiplier: 1

- source: close

- (v) Use EMA

- Bands Style: Average True Range

- ATR Length: 18

- Stop Loss (%): 20

- Take Profit (%) : 5

_________________________________

▶ Usefulness and Originality

- Stop Loss and Take Profit functions are available

- Convenient Buy and Sell entry compared to the original Keltner Channel Strategy

- Optimized for BTCUSD market (maximizing profits)

___________________________________________

이 전략은 TradingView의 Built-in 전략인 Keltner Channel Strategy를 비트코인에 맞게 최적화되었습니다. 기존의 Keltner Channel Strategy는 Buy, Sell 신호가 캔들 중간에 실시간으로 떠서 진입 시점을 예측하기 어려운 불편함이 있었지만 이 전략은 비트코인 가격이 Keltner Channel 상단 혹은 하단을 찍고 종가를 마감하면 그 다음 캔들 시작가에서 Buy 혹은 Sell 진입이 가능하여 편리합니다. 또한, 이 전략은 Keltner Channel을 만나서 캔들을 마감한 가격 (bprice, sprice)을 시각적으로 plot을 제공하여 타점 및 차트를 보기에 편리하며 손절가 및 목표가를 지정한 백테스팅이 가능합니다.

10PreBuyerQuite a simple system

Uses a moving average, the blue line to try and get filled at favorable prices

The MA is multiplied by a number (e.g. .90) which means the system tries to get filled at a 10% lower price (on the Blue MA line)

This means that stop limit buy orders have to be set in advance on the blue line and hope that they would get filled when there is a temporary drop in price

This obviously works best on tickers with a clear long-term up direction

The multiplier can be set to .95 to try and get in on 5% drops instead of 10% drops

"Prof TRG %" determines what profit target you'd like the system to use, default is 1.2 meaning a 20% target, but 1.05, 1.10, and 1.30 would also be good considerations

"Loss TRG %" determines what stop-loss target you'd like the system to use, default is 0.90, meaning 10% stop loss, but, .95, and .85 would also be good considerations

The Profit Target line is green

The Stop Loss target line is red

Using the combination of the Stop Loss inputs and Profit Target inputs you can determine your own RR (Risk to reward ratios), for example, 1:1, 2:1, 3:1, 5:1

Let me know if anything is unclear and I'll try to clarify.

Again, this system assumes that you'll have waiting stop limit orders that are trying to get filled on the blue line, is below price most of the time -- so it's trying to get in on temporary drops on instruments that have a long term uptrend.

1:1 RR ratio would mean high win %

1:5 RR ratios would mean low win %

Not that win % matters, the important things IMO to pay attention to is Profit Factor and a relatively smooth equity cruve

StocasticRSI EMAs ATR StrategyA scalping based strategy thats works well with EUR/USD 30 minute time frame.

This strategy uses stochasticRSI for trade entry. Uses two exponential moving averages for trend detection. The strategy uses Average True Range for stop loss and for two profit targets.

We only trade with the trend if the 50 period exponential moving averages is above the 200 period exponential moving averages. StocasticRSI must cross below 30 level by default for a long entry if the rend is up. Likewise with a short entry the stochasticRSI must crossover above 70 level and if the trend is down.

This script does not trail your stop loss as I have noticed it does not give me good results. Stop loss is a fix stoploss based on Average True Range and so are the profit targets.

This script has risk management, it risk a certain percent of the inputed capital amount in the setting. See settings for more details.

Green line is 50 period exponential moving averages and red line is the the 200 period exponential moving average. Blue line is stoploss for short trade and black line stop loss for buy trade.

Since this is a scalping strategy be caution with the commission and slippage. I have inputed 1 for commission and 1 for sllipage.

Many Thanks,

Honest Trader

[EURUSD60] BB Expansion StrategyOverview

This is a strategy that can be used in the EURUSD 60 time frame.

It is a trend-following method that uses Bollinger Bands Expansions.

The idea of using Bollinger Bands expansion is well known to the general public, but I don’t know any strategy that this idea has been PINE coded.

The three main components of this strategy are as follows.

・Long term BB and Short term BB : When the short term BB expands more than the long term BB, it suggests the occurrence of a trend.

・14EMA of 240 t/f : The direction of 14EMA of the upper time frame is used as the trend direction.

・ATR lines : As a stop-loss line and a take-profit line.

Description

Fig. Long entry pattern

Fig. Short entry pattern

・Description of lines

Gray : Large BB (=Long term BB)

White : Small BB (=Short term BB)

Blue or Red line : Upper t/f EMA(default: 14EMA), blue is up-trend, red is down-trend

Yellow : Stop loss line by ATR(the term is 14)

Purple : Take profit line by ATR(the term is 14)

・Description of strategy

First of all, when the small BB expands more than the large BB, this strategy detects the occurrence of a trend.

Second, When the price crosses over or crosses under small BB basis, this strategy entries long or short to trend direction (by upper time frame 14EMA).

The default stop-loss range is three times ATR value, and the default take-profit target is 1.5 times the stop-loss range (=risk reward ratio is 1.5).

The Box Percent StratHi guys,

Version Zero (more work needed) of an idea I've been meaning to out into a strategy for a while. 🤯

This uses percent boxes🤔 instead of traditional indicators like RSI, MACD etc. 🤫

Takes the first close price of the series and creates a Top Band 10% up, buys if price reaches that level, and puts a stop on a Bot Band, 10% down

When the first trade is in profit by another 10%, it enters another trade and moves the stop of the first trade to breakeven ~ this way it only has one unit of risk at a time

/// Designed for LONG only on Daily, 2D or 3D Charts👌🏻

/// Uses fixed investment risk amount, meaning you're willing to lose that amount per trade

/// Limit buy to not overpay on entries

/// Idea Based on the Darvas system:

/// System only enters trades on strength, when prices equals of exceeds the green line

/// It ads onto the trades, but only *IF* the previous trade is in profit by the UpBoxSize percent size

/// The trailing stop loss is moved up, with the red line

/// A key idea is to only take one unit of risk at a time, meaning for a new add on trade to be taken, the previous trade should be in profit by the same box size as the new new trade's stop loss

/// This will keep adding trades again and again, and they will stop out at the same stop loss

/// Yellow Circles is an MA that filters out choppy areas -- this system only does really well on trending linear markets like: TQQQ, SSO, SPX, SPY

/// Base setting is 10% UpBox Size and 10% DnBox Size: 15% & 15% will be more accurate but fewer signals. 13% profit and 10% stop loss will give a higher risk to reward ratio

Combo Backtest 123 Reversal & MACD Crossover with Trail and Stop

This is a modification of @HPotter "Combo Backtest 123 Reversal & MACD Crossover" script.

I've added a trail stop, basic leverage simulation and stop loss.

Below is HPotter's explanation of the script principals.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

MACD – Moving Average Convergence Divergence. The MACD is calculated

by subtracting a 26-day moving average of a security's price from a

12-day moving average of its price. The result is an indicator that

oscillates above and below zero. When the MACD is above zero, it means

the 12-day moving average is higher than the 26-day moving average.

This is bullish as it shows that current expectations (i.e., the 12-day

moving average) are more bullish than previous expectations (i.e., the

26-day average). This implies a bullish , or upward, shift in the supply/demand

lines. When the MACD falls below zero, it means that the 12-day moving average

is less than the 26-day moving average, implying a bearish shift in the

supply/demand lines.

A 9-day moving average of the MACD (not of the security's price) is usually

plotted on top of the MACD indicator. This line is referred to as the "signal"

line. The signal line anticipates the convergence of the two moving averages

(i.e., the movement of the MACD toward the zero line).

Let's consider the rational behind this technique. The MACD is the difference

between two moving averages of price. When the shorter-term moving average rises

above the longer-term moving average (i.e., the MACD rises above zero), it means

that investor expectations are becoming more bullish (i.e., there has been an

upward shift in the supply/demand lines). By plotting a 9-day moving average of

the MACD , we can see the changing of expectations (i.e., the shifting of the

supply/demand lines) as they occur.

WARNING:

- For purpose educate only

- This script to change bars colors.